Key Takeaways

- Section 404 of the United States’ CLARITY Act[1] bans passive stablecoin yield while preserving activity-based rewards tied to payments and platform usage.

- Crypto equities moved sharply, Circle +30%, Coinbase +9%, BitGo +20%, Galaxy +20%, before the bill became law.

- US spot Bitcoin ETFs recorded $629.8M in net inflows on May 1 during the same week, confirming that regulatory clarity shapes institutional allocation behaviour.

- The bill still needs US Senate Banking markup, a full Senate vote (60 votes required), and presidential signature.

- Capital displaced from passive stablecoin yield is likely to rotate toward tokenised treasuries, money market funds, and regulated investment wrappers.

- This is not a clean crypto win. It narrows yield-led business models and benefits firms with reserves, compliance infrastructure, and payments focus.

This week, Circle is up 30%. Coinbase is up 9%. Bitcoin is above $80,000. US spot Bitcoin ETFs recorded nearly $630 million in net inflows in a single day. And none of this required the [bill] [CLARITY Act] to become law. The CLARITY Act stablecoin yield compromise moved markets before a single senator voted. That is the signal investors should be reading.

The CLARITY Act is the US market-structure bill that proposes to define how crypto assets, stablecoins, exchanges, and intermediaries operate under US federal regulations. The CLARITY Act’s latest compromise, primarily captured in Section 404, seeks to resolve the single largest procedural blocker in the US Senate: whether crypto companies can pay users yield for simply holding stablecoin balances. The answer, now narrowed, has direct consequences for which business models survive the next phase of US digital asset regulation.

[1] Digital Asset Market Clarity Act of 2025 (H.R. 3633

What Is the CLARITY Act?

The CLARITY Act is US federal legislation that establishes a comprehensive regulatory framework for digital assets. It assigns jurisdiction over digital commodities to the US’ Commodities Futures Trading Commission (CFTC), sets rules for crypto exchanges and intermediaries, and, through Section 404, defines the boundary between stablecoin payment instruments and deposit-like yield products.

The bill addresses a fundamental gap in US financial regulation: how to classify and oversee the full spectrum of digital assets, from Bitcoin and Ethereum to stablecoins and tokenised securities. Prior to the CLARITY Act and its companion bill, the GENIUS Act[1], the regulatory status of most crypto assets was determined through enforcement actions rather than statutory clarity, a condition that limited institutional participation, created legal uncertainty for US-incorporated firms, and pushed activity offshore.

The CLARITY Act’s scope is broad. It covers how crypto assets are classified (commodity vs security), which regulator has oversight authority, what obligations apply to exchanges and custodians, and how stablecoins integrate with existing financial infrastructure. It does not replace the GENIUS Act, the two bills work in tandem, with the GENIUS Act handling the mechanics of payment stablecoin issuance and the CLARITY Act handling the broader market-structure architecture.

[1] Guiding and Establishing National Innovation for U.S. Stablecoins Act of 2025

Section 404 Explained: The Stablecoin Yield Compromise

Section 404 of the CLARITY Act is the provision governing stablecoin yield. It prohibits US-regulated crypto platforms from paying passive, savings-account-style interest on stablecoin balances. It explicitly preserves rewards linked to customer activity: payments, transactions, platform usage, loyalty programmes, and trading incentives.

The revised Section 404 language draws a regulatory line that the industry had been negotiating for months. On one side: passive yield, simply holding a stablecoin balance and receiving periodic interest, structurally identical to a savings account. On the other side: activity-based rewards, incentives tied to what a customer does with the stablecoin. The former is restricted. The latter is permitted.

In essence, Section 404 draws a clear regulatory line: stablecoins can support payments, settlement and customer activity, but they cannot freely become unregulated deposit accounts.

This distinction matters because it resolves a direct competitive conflict between banks and crypto firms. Banks hold federally insured deposits and operate under prudential capital requirements. If crypto platforms could freely pay savings-account rates on stablecoin balances, without the same reserve, capital, and insurance obligations, they would attract depositor capital at the expense of the regulated banking system. Section 404 closes that gap while leaving crypto firms a commercial path through activity-based reward design.

The Tillis-Alsobrooks amendment, which formed the basis for the Section 404 compromise, gave the Senate a workable formula: protect bank deposit economics while giving crypto firms a viable tool for customer acquisition and retention. The compromise is not a clean win for either side, banks wanted a broader restriction, some crypto firms wanted full yield flexibility, but it was sufficient to unblock Senate progress.

Why Markets Moved Before the Bill Became Law (5 Days)

| +29.8%

Circle (CRCL) |

+9.1%

Coinbase (COIN) |

+20.0%

BitGo (BTGO) |

+20.0%

Galaxy Digital (GLXY) |

$80K+

Bitcoin spot price |

Circle’s outsized reaction reflects its specific positioning. As a federally focused stablecoin issuer with reserves, compliance infrastructure, and payments distribution, Circle is precisely the type of firm the CLARITY-plus-GENIUS framework is designed to legitimise. Its business model survives Section 404 intact and potentially strengthens relative to offshore competitors who relied on yield as the primary user incentive.

Coinbase’s move reflects the broader thesis: regulatory clarity reduces the legal overhang that has kept some institutional allocators on the sidelines. Exchanges with US compliance structures, custody capabilities, and reporting infrastructure are positioned to benefit when the regulatory framework rewards those investments.

Winners and Losers Under the New Stablecoin Rules

The Section 404 stablecoin yield compromise does not distribute benefits evenly. It creates distinct outcomes for different categories of market participant, based on how much their current business model depends on passive yield as a customer proposition.

| ✓ Positioned to Benefit | X Under Pressure |

|---|---|

|

|

The Broader Product Design Shift

The crypto market spent years selling yield as the primary product. That model created demand, but it also created structural failures, because users often did not understand whether yield came from lending, rehypothecation, leverage, protocol incentives, duration risk, or counterparty risk. Several of the most high-profile crypto collapses of 2022-2026 traced directly to opaque yield mechanisms that obscured those risk sources. Section 404 is, in part, a regulatory response to that pattern. It is an attempt to separate what stablecoins are for, from what investment products are for, and to make that distinction legally enforceable rather than left to disclosure documents.

US regulation now points the market toward a more fundamental separation of functions:

- Stablecoins, movement of money, payments, settlement, dollar rails

- Investment products, yield, with clear risk disclosure and regulatory wrapper

- Exchanges, access, liquidity, price discovery

- Banks, deposits, regulated cash accounts, lending

- Custodians, safekeeping, asset segregation

This separation may reduce some of the product ambiguity that made the previous market cycle fragile. It also increases the cost of operating across multiple of these categories simultaneously without corresponding regulatory authorisation.

The Senate Path: Vote Math and Legislative Chokepoints

The Section 404 stablecoin yield compromise removed the largest procedural blocker, but it did not put the CLARITY Act on the president’s desk. Multiple legislative gates remain, each carrying meaningful passage risk.

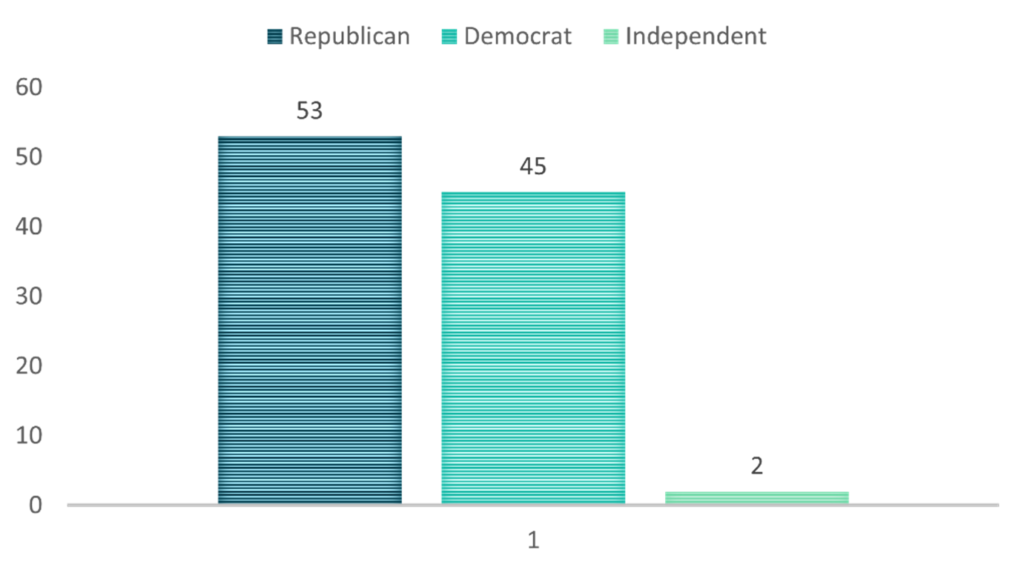

Senate Composition, 119th Congress

Source: 119th United States Congress – Wikipedia

Most major Senate legislation requires 60 votes to invoke cloture (end debate). With 53 Republican seats, the CLARITY Act needs at least 7 additional votes from Democrats or independents to advance. That math is why the Section 404 stablecoin yield compromise mattered: it gave moderate Democrats and banking-aligned legislators a reason to support the CLARITY Act.

Remaining Chokepoints

Senate Banking Chair Tim Scott must schedule a markup before the full Senate can vote. During that markup, the committee must debate the Tillis-Alsobrooks language, process amendments, address developer protection provisions, resolve ethics-related concerns, and vote the bill out of committee. Each of those steps is a potential delay or renegotiation point.

A strong bipartisan Senate Banking markup, multiple Democratic co-sponsors, limited amendments, clean committee vote, would significantly improve CLARITY’s odds in the full Senate. A narrow, party-line markup would signal that the 60-vote threshold remains out of reach. A banking lobby push against the activity-reward language, arguing it creates loopholes that replicate deposit economics through indirect means, could reopen the yield question entirely.

The current market reaction is pricing-in legislative progress, not legislative completion. That distinction matters for anyone sizing positions based on regulatory certainty assumptions.

CLARITY Act vs GENIUS Act: Understanding the Full US Crypto Framework

The CLARITY Act and the GENIUS Act are complementary bills, not competing ones. Understanding the distinction between them is essential to reading the full regulatory landscape.

CLARITY Act vs GENIUS Act, Key Distinctions

| Dimension | CLARITY Act | GENIUS Act |

|---|---|---|

| Primary focus | Broad crypto market structure, classification, exchange rules, CFTC jurisdiction | Payment stablecoin issuance, reserve standards, licensing, AML |

| Stablecoin coverage | Yield and reward rules (Section 404); integrates with GENIUS | Issuer eligibility, 1:1 reserves, audits, consumer protection |

| Regulator | CFTC (digital commodities), SEC (digital securities), shared | Office of the Comptroller of the Currency, Federal Reserve, state banking regulators |

| Who can issue | N/A | Approved banks, credit unions, federally licensed nonbank issuers, qualifying state issuers |

| Key provision | Section 404, stablecoin yield restriction | One‑to‑one reserve requirement with audit and disclosure obligations |

| Legislative status (May 2026) | Senate markup pending; stablecoin yield compromise reached | Passed Senate Banking Committee with bipartisan support |

| MiCA comparison (EU) | Partially analogous to MiCA Title III (asset‑referenced tokens) and Title V (MiCA general provisions) | Analogous to MiCA Title IV e‑money token rules (reserve, redemption, disclosure) |

Europe’s MiCA framework provides the closest available regulatory precedent. MiCA draws a similar distinction between e-money tokens (analogous to payment stablecoins under GENIUS) and asset-referenced tokens, while restricting yield on e-money tokens that could qualify as deposits. The US framework appears to be converging on comparable structural logic, though with different institutional architecture and enforcement mechanics.

The Wider Implications: Tokenised Funds, CFTC Oversight, and Banks

The stablecoin yield compromise is the headline, but the CLARITY Act’s implications extend across the full digital asset stack.

Tokenised Money Market Funds and Treasury Products

Investors who want yield on digital dollars now face a clearer regulatory signal: passive stablecoin interest is restricted; investment products with explicit yield mechanisms are the alternative. Tokenised money market funds and tokenised Treasury products sit inside clearer investment-product wrappers with required risk disclosures, fund structure, and counterparty transparency. The demand that had been flowing into yield-bearing stablecoins has a regulated destination available. The question is how quickly distribution, custody, and on-boarding infrastructure develops to capture it.

CFTC Spot Market Oversight for Digital Commodities

The CLARITY Act assigns CFTC oversight to digital commodities, a category that likely includes Bitcoin and potentially Ethereum. This gives the futures-and-derivatives regulator a spot-market jurisdiction that it has historically lacked, creating a clearer oversight path for commodity-like crypto assets that do not fit the securities framework.

Banks Enter the Digital Asset Infrastructure

Banks now have a stronger incentive to participate in digital asset offerings rather than watching from the sidelines. The emerging rules protect their deposit base from unregulated stablecoin competition while giving them a clearer path into payments infrastructure, tokenised product distribution, and custody services. The question for banks is no longer whether digital assets are permissible, it is how to build the infrastructure and partnerships to compete with crypto-native firms on their terms.

Outlook

The next phase of US crypto regulation will not reward every crypto company equally. It will reward firms that can explain where client money sits, how reserves work, how rewards arise, who regulates the product, and how customers exit in stress. It will pressure firms that rely on vague yield claims, offshore structures, or regulatory arbitrage.

The investor conversation has shifted structurally. The question is no longer whether crypto is allowed. It is: which exposure fits the portfolio mandate, which wrapper fits the compliance framework, and which counterparty can survive the emerging rulebook. That question now has more inputs to work with than at any previous point in the asset class’s history.

Regulated wrappers, spot ETFs today, potentially tokenised funds tomorrow, are the primary instrument through which institutional allocators will access this asset class. ETF flows have already demonstrated this: when access, custody, and regulatory framing align, capital follows. The CLARITY Act, if it passes, extends that dynamic from Bitcoin to stablecoins, digital commodities, and eventually tokenised yield products.

The US has not removed crypto risk. It has started to define where different categories of risk belong. A defined risk is a priceable risk. That is the fundamental change this legislative cycle represents, and why markets moved before the bill became law.

Disclaimer – Research and Educational Content

This document has been prepared by AMINA (Austria) AG (“AMINA EU”). AMINA EU is a Crypto-Asset Service Provider with its head office and legal domicile in Austria. It is authorized and regulated by the Austrian Finanzmarktaufsichtsbehörde (FMA).

This document is published solely for educational purposes; it is not an advertisement nor a solicitation or an offer to buy or sell any financial investment or to participate in any particular investment strategy. This document is for publication only on AMINA EU website, blog, and AMINA EU social media accounts as permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA EU to any registration or licensing requirement within such jurisdiction.

Research will initiate, update and cease coverage solely at the discretion of AMINA EU. This document is based on various sources, incl. AMINA EU ones. In preparing this document, AMINA EU may have made limited use of artificial intelligence–enabled tools to assist with research, summarisation, and drafting, with all content subject to human review and validation.

No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA EU. The information is not intended to be a complete statement or summary of the subjects alluded to in the document, whereas general information, financial investments, markets or developments. AMINA EU does not undertake to update or keep current information. Any statements contained in this document attributed to a third party represent AMINA EU’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any formulas, equations, or prices stated in this document are for informational or explanatory purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been affected at those formulas, equations, or prices, and any formula(s), equation(s), or price(s) do not necessarily reflect AMINA EU’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA EU or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances or otherwise constitutes a personal recommendation. Investments involve risks, and investors should exercise prudence and their own judgment in making their investment decisions. Financial investments described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including, among others, deposit, buy, sell or hold investments) made by AMINA EU and its employees may differ from or be contrary to the opinions expressed in AMINA EU research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA EU. Unless otherwise agreed in writing, AMINA EU expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA EU accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

©2026 AMINA (Austria) AG, Seestrasse 6/13, 6900 Bregenz, Austria, FN 631729p, Landesgericht Feldkirch